How to Save Money on Taxes for Your Business?

As business owners get caught up in running their business, they still have to be concerned with paying taxes. Despite the fact that they already have to wear several hats, being sensitive to what’s happening to their tax situation is critical. In fact, it’s important to take a look at your tax situation before the tax year ends. In doing so you can identify tax strategies to see how you can save money on taxes. This allows you to make adjustments during the tax year.

But what steps can you take that will allow you to save money on taxes? Are you overlooking legitimate business expenses that you could legally write off to reduce taxes? Are you making the right decisions that have the best tax outcome for your business? What about your business entity? Do you have the best business structure that will save you the most in taxes?

If you are looking for answers to these questions, continue reading. Below is more information about how to keep more of your hard-earned money in your business.

Understand the Tax Implication Of Your Business Structure

Many business owners are completely unaware of how their business structure impacts their tax liability. Some business owners aimlessly select a business structure without digging into the pros and the cons or weighing the benefits in general.

For example, if you operate as a sole proprietor, your profits and losses are pass-through to your personal taxes and there is no double taxation.

However, if you have a C corporation not only will you have to pay corporate income taxes, but you also have to pay taxes on dividend distributions. This is referred to as double taxation. More specifically double taxation means basically being taxed on the same source of income twice.

So even if you find ways to save money on taxes in general, you may find that you’re still paying more taxes than you have to based on your business structure. So which business structure should you select to get the best tax benefit? Read on. More information about this is provided below.

The Four Main Types of Business Structures

Before we talk about which corporate structure provides the best tax benefits, we will first touch on the main types of business structures that are available in the U.S:

- Sole proprietorship

- Partnership

- Limited Liability, and

- Corporation

Each of these four main structures has a different type of tax liability implications. Setting up the proper structure based on both your business activities and knowing which structure helps you save money on taxes is critical. The earlier you set up the right business structure the more money you will save.

What Type of Business Structure Saves the Most on Taxes?

Filing taxes is extremely confusing for small business owners and entrepreneurs. To add to the confusion, there are also changes in the tax laws, which can have an additional impact on your taxes. It’s important to think through, which entity is best for you sooner rather than later.

As indicated above there are four main business entities that can be structured in the U.S. However, selecting the right business structure can help your business pay the least in taxes. Knowing the differences between them can be very helpful too. Below is more information on which business structure can help you save money on taxes.

Sole proprietorship

If you set your business up as a sole proprietor, both the business entity and the owner are one in the same. The business is not a taxable entity according to the IRS. As a result, all of your profits and losses will be passed through to your personal tax returns on form 1040. You will be responsible for reporting your expenses on schedule C and filing the profits or losses with your personal income tax returns. In other words, your business taxes is passed to your personal income taxes.

The impact on your taxes will be determined by whether or not you had a profit or loss in your business. Other factors will also be determined that could further reduce your business tax liability.

General Partnerships

Just like the sole proprietorship business structure, the general partnership is not considered a taxable entity. As a result there is no separate income tax return for the partnership. However, the income from the partnership is passed through or distributed to the partners and will be taxed on their individual returns.

Limited Liability

A limited liability company is a separate legal entity under most state laws. The owners are provided with a form of liability protection and also have the pass-through tax structure, meaning that the LLC does not have to prepare or file taxes on behalf of the business. However, the income and losses are reported on the personal income tax returns and paid by the individual members of the LLC.

Corporation

The tax implications of a C corporation requires the corporation to be set up as a separate entity. This requires the corporation to be taxed separately from its shareholders who must also pay taxes when they receive their dividend distributions.

A C Corporation must pay taxes as a corporate entity as well as the individual shareholders, which is referred to as double taxation. What that means is that the income that is earned by the C corp is taxed using the latest corporate tax rates and the net profits that are generated are distributed to the owners which is also taxed.

If a company plans to go public they normally set up a C corporation. The net income is taxed and as indicated each of the individual shareholders who purchased shares of stock in a public stock trade must also pay taxes individually.

If you elect to have an S corporation, it requires a special election with the IRS. This election allows the C corporation to be treated as a partnership or like an LLC for tax purposes. The corporation itself is not subject to income tax but is also considered a pass-through entity.

If you find that there is a different business structure that’s more beneficial to your current tax situation. You can consider changing your business structure to a different entity.

How To Save Money Each Month On Taxes With the Decision You Make

In addition to saving money on taxes based on the type of business entity you set up, you can also find ways to save money on taxes each month. The business decisions you make can have a significant impact on how much money you pay in taxes. That is why it’s important to sit with a tax preparer or an accountant to talk about some strategies that you can implement that will save you the most money.

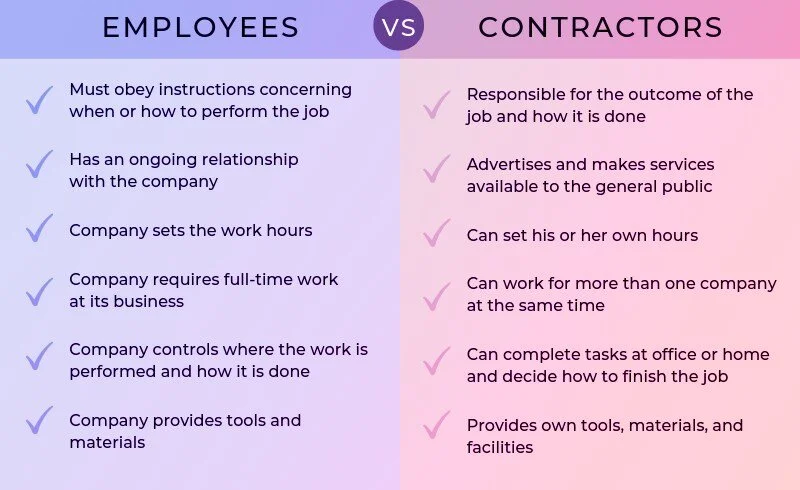

Hiring Staff Versus Independent Contractors

When trying to save money on taxes, one of the things to keep in mind are the cost differences when hiring an employee versus outsourcing to an independent contractor.

Hiring Staff

When you hire staff members, with it comes a wide variety of expenses. For example, if you have a physical brick and mortar location, you will be required to pay for general liability insurance, workers comp insurance and other types of insurance based on your state’s laws.

These insurances are required based on the assessed risk that is associated with each staff member as they perform their job function at your site location.

In fact, each job function is classified based on a risk level which is used to determine the likelihood of there being an occupational accident based on the job function performed.

Hiring Remote Staff

If you hire an employee, but they work remotely, or only come into the office occasionally, you will be able to save some money. However, there are other taxes involved with hiring employees such as payroll taxes. These taxes can really add up and can easily impact your out-of-pocket cost on a monthly, quarterly or annual basis.

Depending on the state where your business is located, you will likely also have to pay both state and federal payroll taxes.

Medical and Health Benefits

To maintain good staff members most of them require some form of medical and health benefits. When this is part of the employment offer you may get a bigger commitment, however it may cost more money during the year. Some of these benefits include the following indicated below:

Paid Leaves

Most employers are also responsible for providing paid leaves such as medical leaves for an extended period of time, sick leaves, vacation leaves, military leaves, and so forth. These are other cost factors that should be considered.

Bonuses

Paying bonuses to staff members also requires employers to shell out money that could ultimately have an impact on your taxes. You’d have more expenses that would reduce your tax liability. But here again, the idea is to find out if this strategy keeps more money in your pocket.

Onboarding Cost

When hiring staff members there’s also additional costs associated with attracting and bringing new staff members on board. These calls could consist of advertising costs, background checks, orientation, and training costs, and sometimes sign on bonuses.

Although this influx of out of pocket expenses can reduce your tax liability, it does get expensive and can reduce your net profits. Although the goal is to learn ways to save on taxes the ultimate goal is to find ways to save money overall as well as save money on taxes.

Outsourcing and Hiring Independent

If you decide to hire an independent contractor instead of an employee, you can save money in a lot of ways. For example, you will not be responsible for medical and health insurance, payroll taxes, employee onboarding costs as well as other employee related expenses.

Although this approach will likely keep more money in your pocket it will result in you having higher net profits which means that you may have to pay higher income taxes. However, if you look at the big picture and the overall bottom line this could reduce your overall spending in general.

That’s why it’s important to weigh the pros and the cons and determine which method is most practical for saving you money and ultimately reducing your taxes.

Writing Off Expenses

There are other ways that you can save money on taxes by simply writing off expenses that you already have. If your business consists of certain activities that help you do business and generate sales you can write them off to reduce your tax liability. Are you overlooking some legitimate tax write off‘s? Here are a few that could help you further reduce your tax liability:

Travel Expenses

If you travel a lot for a business you will likely be able to reduce your taxes by writing off your travel-related business expenses. Most business travel-related expenses are fully deductible as long as there is a justifiable business related purpose for your travel. Some of those expenses consist of the following.

Air fare

Local travel-related expenses

If you need to travel locally for legitimate business purposes, you can also write off those expenses as well. Typical local business expenses include

Mileage Expense

The IRS does allow you to track your mileage expenses, although there may be some limitations on how much you can deduct. Even if you use your personal vehicle, as long as the trip is for business purposes, you are allowed to write off the actual amount spent for gasoline.

The IRS does require that you record and keep track of your miles, however. You can use one of the following methods:

Actual Expense Method

The IRS allows you to add up all of the actual expenses that you spent on gasoline to travel for business purposes.

Odometer Method

Using the odometer method, you can record how many miles you traveled for business purposes by logging the total miles of each business trip.

You will need to make a record of your odometer reading at the beginning of the year. So what that means is that on January 1st you need to record the odometer reading as well as at the end of the year on December 31st. Your tax preparer will then use the total miles for the year, and determine

how many miles were used for commuting

how many miles were used for business purposes, and

how many miles were used for personal use

In order to provide your tax preparer with accurate information, it’s important for you to maintain a record of your business trips throughout the year as well as the beginning and ending odometer reading. When you maintain accurate information throughout the year, it’s easier for you to provide the information needed to your tax preparer at the end of the year.

What Information is Required by the IRS?

If you plan to write off mileage expenses on your tax return the IRS requires you to maintain a mileage log that must include the following:

The total miles driven pro trip

The dates of the business trip

Where you drove

The purpose of the trip

When Can Mileage Expenses be Deducted?

You can write off mileage expenses when you drive to meet with clients, attend business meetings, attend business events such as conferences, seminars, and business-related networking meetings, or to pick up supplies.

Tools and Resources

When using apps to track your mileage they should be IRS compliant mileage tracker‘s such as those indicated below.

TripLog

MileIQ

Everlance

QuickBooks Self Employed

Transportation Expenses

You cannot write off commuting expenses to get to your job. However, if you are a business owner I need to travel for legitimate business purposes, you can use write off transportation expenses to save money on taxes.

Some of the most common transportation expenses consist of

Cab Fare,

Uber and Lyft

Although expenses associated with cab fare were a lot more popular some years ago, it’s still a legitimate business expense when used for business purposes. However, many people have turned to Uber and Lyft. They have become popular forms of transportation and is also deductible as long as it is for a legitimate business purpose

It Is Possible To Save Money. Trust the Billry Shop.

Parking Expenses

If you drive to a business meeting or to meet with a prospective client, you will likely need to pay for parking. If so, you can include this in your travel related expenses.

Depreciation

If your business has capital expenditures for items such as vehicles, or business equipment, the IRS allows you to write off the loss of value of these items over the life of the asset.

This process is called depreciation expense and they can be applied to your expenses to reduce your taxes. You’ll need to find a method that’s appropriate for your business and use the same annually. Otherwise you will have to communicate with the IRS about any changes that you would like to make.

The most commonly used depreciation method is the straight line method. However other methods include the double declining balance, units of production and the sum of years digits. Additionally, the IRS allows business owners to write off a large portion of their depreciation in the year that the asset was purchased. It is referred to as Section 179. For more info for more detailed information on these on depreciation methods, and which one is best to save money on taxes for your business consult with your tax professional or accountant.

Retirement Plans

As a small business owner, you also have the opportunity to participate in the wide variety of retirement plans known for providing tax benefits/reducing taxes. However, this wide variety of tax benefits for business owners that may require some forethought and planning. Some of the popular options include a:

- SEP IRA

- Simple IRA

- Independent 401(k)

Conclusion

If you've been wondering how can I save money on taxes and in your business, you can now see that there are many ways that you can save money on taxes for your business. It basically takes planning and forethought during the tax year. You may consider opening a savings account, to help you save more money. You can also take advantage of a wide array of business tax credits that will help your business save even more money.